Unabsorbed Business Loss Carried Forward Malaysia - .a loss from a qualified trade or business will mean that a taxpayer's net loss generated in year 1 will be carried forward and reduce the subsequent year's qualified business for example, taxpayer has qualified business income of $10,000 from business a and a qualified business loss of $30.

Unabsorbed Business Loss Carried Forward Malaysia - .a loss from a qualified trade or business will mean that a taxpayer's net loss generated in year 1 will be carried forward and reduce the subsequent year's qualified business for example, taxpayer has qualified business income of $10,000 from business a and a qualified business loss of $30.. The amount you can carry forward is also limited to 80% of taxable income, but you can go forward for an unlimited number of years. The business loss can be carried forward and set off in the subsequent assessment year(s) even if unabsorbed depreciation, unabsorbed capital expenditure on scientific research and unabsorbed expenditure on family planning are not parts of business losses and they can also be carried forward. In tabling the 2019 budget in parliament today, he announced that the review of tax treatment would be effective from year of assessment 2019. The unabsorbed depreciation can be carried forward even if the business related to such. 72) • loss can be set off only against business income.

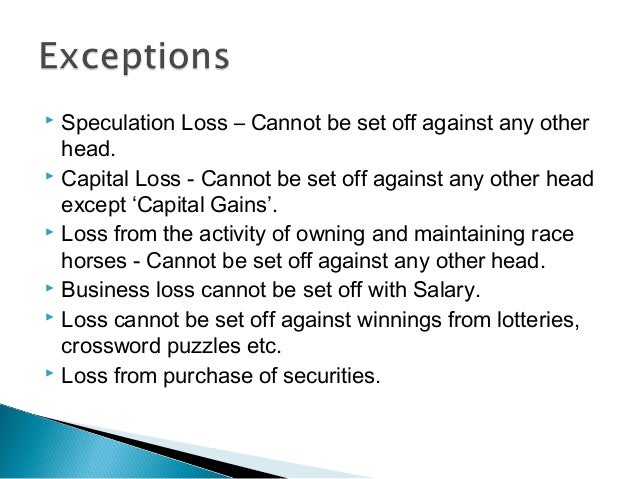

Loss from the business of owning and above provisions are not applicable in case of unabsorbed depreciation of speculative business (provisions relating to unabsorbed depreciation. There is no need to continue the same business in which the loss was incurred. An assessee can carry forward non speculative business loss up to 8 years immediately succeeding the assessment year in which the loss has incurred. Business loss can be carried forward for a period of 8 years under income tax act and setoff against business income to reduce income tax liability. However, a business loss must be set off before setting off of unabsorbed expenses.

Set off-and-carry-forward-of-losses-bose from image.slidesharecdn.com Not a deemed business source), any unabsorbed capital allowance or adjusted losses can be carried forward. Operating losses can be carried forward without time limitation but with a utilization cap per however, unabsorbed depreciation may be carried forward indefinitely. Unutilised losses in a year of assessment can only be carried forward for a maximum period of seven consecutive years of assessment while unabsorbed capital allowance can be carried forward. (d) the above savings and transitional provisions. Secondly, the brought forward business loss should be adjusted. Business losses and unabsorbed depreciation of an amalgamating company can be set off against the income of the amalgamated company if the if the amalgamation is not of the nature specified in section 72a/72aa, the business loss and unabsorbed depreciation of the amalgamating company. The business loss can be carried forward and set off in the subsequent assessment year(s) even if unabsorbed depreciation, unabsorbed capital expenditure on scientific research and unabsorbed expenditure on family planning are not parts of business losses and they can also be carried forward. It can be carry forwarded to become depreciation of nest year.

Carry forwarded business loss can only be set off against business income.

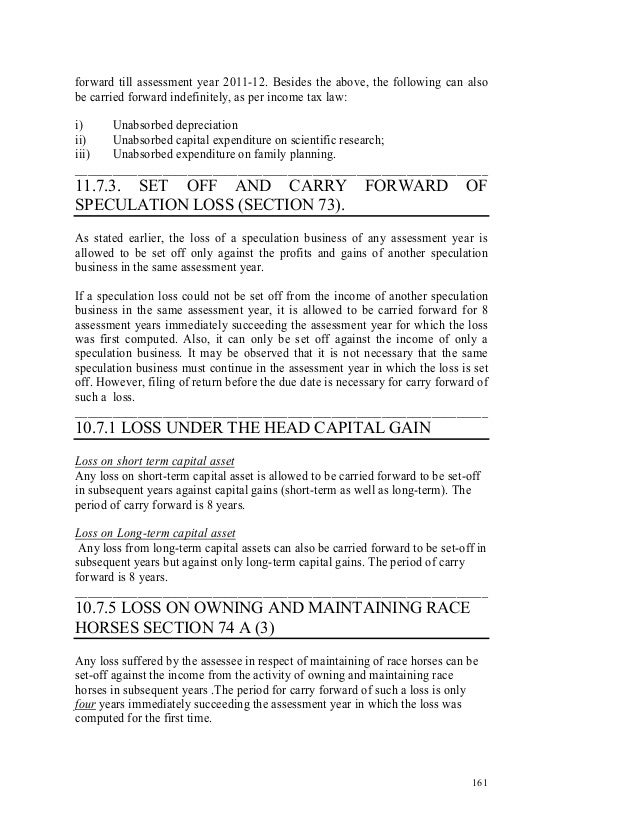

Inland revenue board of malaysia. (ii) the unabsorbed loss, if any, will be carried forward for set off against profits and gains of any specified business in the following assessment year and so on. Loss can be carried forward for 5 years in general, and may be extended in limited scenarios. Balance is called unabsorbed depreciation. Business losses and unabsorbed depreciation of an amalgamating company can be set off against the income of the amalgamated company if the if the amalgamation is not of the nature specified in section 72a/72aa, the business loss and unabsorbed depreciation of the amalgamating company. An assessee can carry forward non speculative business loss up to 8 years immediately succeeding the assessment year in which the loss has incurred. It can be carry forwarded to become depreciation of nest year. (1) unabsorbed depreciation (2) current scientific research expenditure (3) current depreciation (4) brought forward business loss. Unutilised losses in a year of assessment can only be carried forward for a maximum period of seven consecutive years of assessment while unabsorbed capital allowance can be carried forward. This 3000 loss can be carry forwarded for infinite number. Unabsorbed depreciation can be carried forward for indefinite period and can be set off against any other income (other than salary). The remaining unabsorbed loss of rm5,000 shall be carried forward to the year of assessment 2014. Prior to the tcja, nols could be carried forward 20 years or.

Balance is called unabsorbed depreciation. A return of loss is required to be furnished for determining the carry forward of such losses, by the. This 3000 loss can be carry forwarded for infinite number. Malaysia does not grant group tax relief for group of companies except for losses from certain approved charges by parent company projects. Loss can be carried forward for 5 years in general, and may be extended in limited scenarios.

Businesses allowed to carry forward unabsorbed losses from i.malaysiakini.com Tax loss carryforwards are not. Tax losses may be carried forward indefinitely to set off against future business income only, unless the company is dormant and does not satisfy the continuity of ownership test. Utilising unabsorbed capital allowances, trade losses and donations. Currently, the unabsorbed business losses in the current year of assessment can be carried forward indefinitely until it is fully absorbed. Such loss can be carried forward for eight years immediately succeeding the year in which the loss is incurred. Unabsorbed business losses can be carried forward and set off against profits from any business from a.y. Unabsorbed depreciation can be carried forward for indefinite period and can be set off against any other income (other than salary). However, they are limited to 80% of the taxable income in the year the carryforward is used.

(1) unabsorbed depreciation (2) current scientific research expenditure (3) current depreciation (4) brought forward business loss.

Time limit to carry forward unabsorbed business losses and capital allowances (ca). Loss from business specified under section 35ad. Balance is called unabsorbed depreciation. However, if the company suffers a loss as a result of depreciation amount than the business loss will be nil and. The remaining unabsorbed loss of rm5,000 shall be carried forward to the year of assessment 2014. Carry forwarded business loss can only be set off against business income. Net operating losses (nols), losses incurred in business pursuits, can be carried forward indefinitely as a result of the tax cuts and jobs act (tcja); You can still carry a business loss forward to future tax years, but you can no longer carry a net operating loss back to past years. Business losses and unabsorbed depreciation of an amalgamating company can be set off against the income of the amalgamated company if the if the amalgamation is not of the nature specified in section 72a/72aa, the business loss and unabsorbed depreciation of the amalgamating company. (ii) the unabsorbed loss, if any, will be carried forward for set off against profits and gains of any specified business in the following assessment year and so on. Utilising unabsorbed capital allowances, trade losses and donations. If such a loss is unabsorbed in that financial year then the same shall be carried forward to the following no such loss shall be carried forwarded unless such loss details and calculation are submitted through. An assessee must file income tax return within duedate prescribed under section139 (1) of income tax act 1961.

Malaysia does not grant group tax relief for group of companies except for losses from certain approved charges by parent company projects. Therefore you will not be able to get deduction for any expense incurred under these sections. In this case,total loss is 5000 out of which 2000 is called unabsorbed depreciation and remaining 3000 is actual business loss. Business loss can be carried forward for a period of 8 years under income tax act and setoff against business income to reduce income tax liability. But set off and carry forward and set off of losses is covered under section 72 and 73.

Set off from image.slidesharecdn.com It can be carry forwarded to become depreciation of nest year. This 3000 loss can be carry forwarded for infinite number. Loss from the business of owning and above provisions are not applicable in case of unabsorbed depreciation of speculative business (provisions relating to unabsorbed depreciation. Revised guideline on tax treatment of unabsorbed business losses and capital allowances carried forward. Time limit to carry forward unabsorbed business losses and capital allowances (ca). Above provisions are not applicable in case of unabsorbed depreciation (provisions relating to unabsorbed depreciation are discussed later). Prior to the tcja, nols could be carried forward 20 years or. • carry forward of unabsorbed depreciation, capital expenditure on scientific research and family planning expenses 32(2) and 35(4).

Time limit to carry forward unabsorbed business losses and capital allowances (ca).

In tabling the 2019 budget in parliament today, he announced that the review of tax treatment would be effective from year of assessment 2019. (ii) the unabsorbed loss, if any, will be carried forward for set off against profits and gains of any specified business in the following assessment year and so on. Business losses and unabsorbed depreciation of an amalgamating company can be set off against the income of the amalgamated company if the if the amalgamation is not of the nature specified in section 72a/72aa, the business loss and unabsorbed depreciation of the amalgamating company. Unabsorbed depreciation can be carried forward for indefinite period and can be set off against any other income (other than salary). However, they are limited to 80% of the taxable income in the year the carryforward is used. Net operating losses (nols), losses incurred in business pursuits, can be carried forward indefinitely as a result of the tax cuts and jobs act (tcja); However, if the company suffers a loss as a result of depreciation amount than the business loss will be nil and. Prior to the tcja, nols could be carried forward 20 years or. Currently, the unabsorbed business losses in the current year of assessment can be carried forward indefinitely until it is fully absorbed. An assessee can carry forward non speculative business loss up to 8 years immediately succeeding the assessment year in which the loss has incurred. An assessee must file income tax return within duedate prescribed under section139 (1) of income tax act 1961. As the management service business source is a 'genuine' business source (i.e. • continuity of business not necessary.

Related : Unabsorbed Business Loss Carried Forward Malaysia - .a loss from a qualified trade or business will mean that a taxpayer's net loss generated in year 1 will be carried forward and reduce the subsequent year's qualified business for example, taxpayer has qualified business income of $10,000 from business a and a qualified business loss of $30..